|

[Under Section 45ZL of the Reserve Bank of India Act, 1934] The sixty first meeting of the Monetary Policy Committee (MPC), constituted under Section 45ZB of the Reserve Bank of India Act, 1934, was held during June 3 to 5, 2026. 2. The meeting was chaired by Shri Sanjay Malhotra, Governor and was attended by all the members – Dr. Nagesh Kumar, Director and Chief Executive, Institute for Studies in Industrial Development, New Delhi; Shri Saugata Bhattacharya, Economist, Mumbai; Professor Ram Singh, Director, Delhi School of Economics, Delhi; Dr. Poonam Gupta, Deputy Governor in charge of monetary policy and Shri Indranil Bhattacharyya, Executive Director (the officer of the Reserve Bank nominated by the Central Board under Section 45ZB(2)(c) of the Reserve Bank of India Act, 1934). 3. According to Section 45ZL of the Reserve Bank of India Act, 1934, the Reserve Bank shall publish, on the fourteenth day after every meeting of the Monetary Policy Committee, the minutes of the proceedings of the meeting which shall include the following, namely:

4. In the light of evolving developments on the global and domestic front, the MPC reviewed in detail the staff’s macroeconomic projections that included inputs from survey results and stakeholder consultations. The MPC also reviewed alternative scenarios around various risks to the outlook. Drawing on the above and after extensive discussions on the stance of monetary policy, the MPC adopted the resolution that is set out below. Resolution 5. The Monetary Policy Committee (MPC) held its 61st meeting from June 3 to 5, 2026, under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Poonam Gupta and Shri Indranil Bhattacharyya attended the meeting. 6. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.25 per cent. Consequently, the standing deposit facility (SDF) rate remains at 5.00 per cent and the marginal standing facility (MSF) rate and the Bank Rate remain at 5.50 per cent. The MPC also decided to continue with the neutral stance. Growth and Inflation Outlook Global Outlook 7. As the West Asia conflict prolongs without any meaningful resolution in sight, risks to both inflation and growth have increased. Energy markets have been volatile; crude oil reserves are declining and global commodity prices have firmed up. Faced with difficult trade-offs, monetary policy has turned more cautious. Major advanced economy central banks are likely to pivot towards monetary policy tightening. Global financial markets have shown mixed trends, with equities remaining buoyant driven by AI optimism, while sovereign bond yields have hardened on fiscal sustainability concerns and inflation worries. The US dollar index has appreciated recently amid shifting rate expectations and changing risk sentiment. Domestic Outlook 8. As per several high frequency indicators, domestic economic activity remained largely steady since the outbreak of the conflict. Private consumption has been resilient, while fixed investment maintained its momentum despite cost pressures. Merchandise exports recorded strong growth in April 2026, though elevated freight and insurance costs remain a drag. Services exports continued to be robust. While the economy has withstood the conflict spillovers with limited impact so far; the strains are increasingly becoming visible. 9. Looking ahead, elevated energy and other commodity prices coupled with continued supply disruptions are likely to affect economic activity. While import diversification in affected commodities has helped in improving supply, it comes at a higher cost. The full impact, however, will depend on the duration of the conflict, time taken for normalisation of supply chains and the burden-sharing approach among the stakeholders. The south-west monsoon is expected to be deficient, with implications for agricultural activity and rural demand. However, the programmes and initiatives for crop diversification, water harvesting and conservation, climate-resilient practices and short-duration crops, among others, are expected to mitigate the impact. Furthermore, sustained momentum in services, continuing impact of GST rationalisation, and broadly stable employment conditions should continue to support urban consumption. Strong capacity utilisation, sustained credit flows from bank and non-bank sources, and the government’s capex are expected to support investment activity. While weak global demand and elevated freight and insurance costs are headwinds for merchandise exports, services exports are expected to remain steady. 10. Several measures undertaken by the Government, including support to MSME and export sectors, efforts to ramp up domestic gas and crude supplies, encouraging use of domestically produced alternatives to imported inputs, and diversification of critical imports have strengthened the economy’s resilience to cope with external shocks. 11. Taking all these factors into consideration, real GDP growth for 2026-27 is projected at 6.6 per cent, with Q1 at 6.6 per cent; Q2 at 6.3 per cent; Q3 at 6.5 per cent; and Q4 at 6.8 per cent (Chart 1). Prolonged global supply chain disruptions, heightened volatility in global financial markets, and weather-related shocks continue to pose downside risks to the domestic growth outlook. 12. Headline CPI inflation inched up to 3.4 per cent in March and 3.5 per cent in April 2026 primarily due to higher food inflation. Fuel inflation remained modest as retail fuel prices largely remained unchanged in March and April despite the sharp spike in international energy prices. Core (CPI excluding food and fuel) inflation remained unchanged at 3.7 per cent during January to April. Excluding precious metals, core inflation remained much lower at 2.1-2.2 per cent. This indicates that the input cost pressures, as reflected in a sharp increase in April WPI, have not yet fully manifested in CPI. 13. Since May, however, retail fuel prices have been raised cumulatively by 7.4 per cent for petrol and 8.4 per cent for diesel. The increase implies a direct impact of about 36 basis points on headline inflation, which, along with second order effects, would get reflected in CPI inflation in the coming months. Pass-through of higher global energy prices are also visible in several other inputs such as commercial LPG, industrial raw materials, chemicals, rubber and plastic products. The second-round impact of higher input costs could exert upside pressure on CPI inflation going forward. 14. Considering all these factors, CPI inflation for 2026-27 is projected to be 5.1 per cent with Q1 at 4.2 per cent; Q2 at 5.1 per cent; Q3 at 5.9 per cent; and Q4 at 5.4 per cent. Core inflation is projected at 4.7 per cent for 2026-27 (Chart 2). Excluding precious metals, core inflation is projected to be lower, suggesting that demand pressures remain contained. These forecasts are subject to upside risks due to global supply chain disruptions and uncertainty about the spatial and temporal distribution of monsoon. However, adequate stock of foodgrains and satisfactory reservoir levels provide some comfort.  Rationale for Monetary Policy Decisions 15. The global environment has deteriorated since the last policy meeting with the conflict lingering amidst a fragile truce. The adverse implications of the extended disruption in supply chains and elevated energy prices are reflected in the moderation of growth and increase in inflation projections from the April policy as discussed above. 16. CPI inflation remains below the target despite the global shock as the passthrough to domestic prices has been limited. While the baseline projections point towards headline inflation firming up towards the upper tolerance level in Q3:2026-27, the impact of the supply shock is expected to wane Q4 onwards. The underlying inflation pressures continue to remain benign at this juncture. However, generalisation of inflation through second-round effects on expectations and wages is a distinct possibility, warranting a close vigil. The outlook also remains clouded by the sub-normal south-west monsoon forecast and El Niño risks. 17. As for growth, elevated energy prices coupled with global supply constraints are having adverse spillovers on economic activity. While domestic demand remains resilient and manufacturing and services sectors activity continue to expand, there are incipient signs of moderation in some sectors as suggested by high frequency indicators. 18. As discussed above, there are considerable risks to the MPC’s baseline assessment of inflation and growth due to the uncertainty about the duration and intensity of the conflict, magnitude of its spillover effects and the pace of restoration of supply chains. Additionally, the food outlook remains uncertain on account of the sub-normal south-west monsoon forecast and El Niño. Although risks of higher inflation have amplified, the MPC felt it would be prudent to wait for greater clarity to emerge. Accordingly, the MPC voted to keep the policy rate unchanged. At the same time, the MPC will continue to remain data-dependent and closely monitor the developments, including supply side pressures getting embedded in the general price level and inflation expectations. The MPC also decided to retain the neutral stance. 19. The minutes of the MPC’s meeting will be published on June 19, 2026. 20. The next meeting of the MPC is scheduled for August 3 to 5, 2026. Voting on the Resolution to keep policy repo rate unchanged at 5.25 per cent

Statement by Dr. Nagesh Kumar 21. The West Asia conflict and the blockade of the Strait of Hormuz have created a challenging situation for the global economy. The crude prices have shot through the roof, and supplies have been disrupted. The Indian economy has also been affected, given its heavy dependence on imports of hydrocarbons and fertilisers, a substantial proportion of which are routed through the Strait. The rising crude prices raise concerns about consumer prices directly and indirectly, given the dependence of many sectors of manufacturing on petroleum products as fuels and feedstock, even though the government has allowed only a limited pass-through, so far. The Gulf region is also an important destination for India’s exports and a major source of remittances. In addition, there are concerns on the agricultural front arising from El Niño affecting the monsoons. The global uncertainty has also led to outflows of foreign portfolio investments from India, bringing the exchange rate of the rupee under pressure, besides concerns about the balance of payments impact of rising crude prices. Therefore, the West Asia conflict is an important shock for India’s economic outlook in the near term. 22. The Indian economy, however, has entered this crisis with much stronger macroeconomic fundamentals than most previous economic crises (including the global financial crisis, the taper tantrum, or Covid-19). Before the conflict started at the end of February, the Indian economy was enjoying a ‘goldilocks moment’ of robust growth and very benign inflation. Healthy foreign exchange reserves of nearly $700 billion covering about 11 months of imports, and a moderate current account deficit, underpinned by resilient merchandise exports, and buoyant services exports and invisibles. Reservoir levels holding above 20% higher water than the 10-year average, could help to mitigate the possible shortfalls in the monsoon. In any case, over time, Indian agriculture has tended to be less affected by monsoon fluctuations with growing resilience. 23. Emphasis on fiscal consolidation over the past years has helped in bringing down the fiscal deficit from 6.5% of GDP in 2022-23 steadily to 4.4% by 2025-26. This provides some fiscal space to address the challenges posed by the West Asia crisis, including through supporting economic growth by sustaining and even enhancing public investment to mitigate any weaknesses in private consumption due to rising costs and to absorb rising subsidies for absorbing the high crude prices. The private investment sentiment may also be affected due to cost pressures and supply chain disruptions resulting from the West Asia conflict, and may need to be mitigated by enhanced public investment. 24. The weakening of the global economy in the face of the crisis may adversely affect the demand for India’s exports, particularly in the Gulf region. On the positive side, the free trade agreements (FTAs) that India has signed recently with the EU and UK, among other countries, which begin to be implemented in the current year, may help to mitigate some loss of export demand due to subdued demand elsewhere, especially in labour-intensive sectors. 25. Notwithstanding the factors that make the Indian economy better equipped to withstand the current shock than the previous ones, the economic outlook has been adversely affected. The growth projection for 2026-27 at 6.6% is 100 basis points lower than the 2025-26 growth rate of 7.6% (the second advance estimates). The CPI headline inflation is projected at 5.1% for 2026-27, representing a 300-basis point increase over the very benign rate of 2.1% for 2025-26. These projections are obviously subject to a lot of uncertainties surrounding the duration of the West Asia conflict. Even with the lower growth projections, the Indian economy will continue to remain the fastest-growing major economy. The crisis has also reminded on the urgency of accelerating the pace of clean energy transition, fully harnessing the potential of solar, wind, geothermal, biofuels, and nuclear energy to reduce its vulnerability to oil price volatility. 26. In the highly uncertain current economic environment, however, prudence requires waiting for greater clarity to emerge on the impact before any monetary policy response. One needs to keep an eye on the evolving geopolitical situation in West Asia and its implications for the Indian macroeconomic outlook, especially the growth-inflation dynamics. Hence, I vote for the status quo on the repo rate. I also support maintaining the neutral stance. Statement by Shri Saugata Bhattacharya 27. In the two months since the last MPC review in April 2026, the balance of risks, emanating largely from the conflict in West Asia and related geopolitical repercussions, while not having changed materially, now seems to have tilted towards embedding inflationary pressures. For the reasons outlined below, I continue to believe that the outlook for the growth–inflation trade-off in India remains clouded.

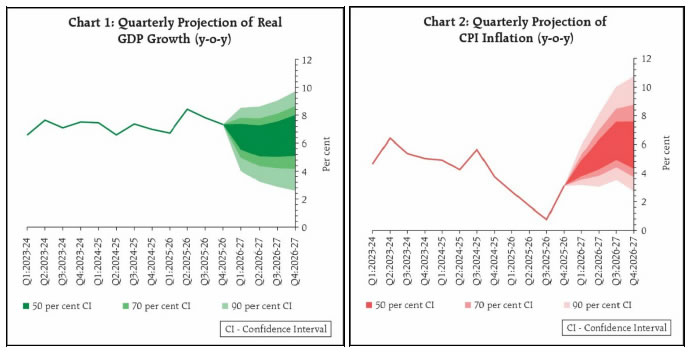

28. In my April 2026 statement, I had noted that “domestic financial conditions have tightened significantly, which amounts to a de facto policy tightening” amidst the risk of accumulating inflationary pressures. Trends in domestic financial markets as of early June 2026 suggest that these tight conditions continue, obviating the need for additional tightening via the policy repo rate. 29. Given the multiple overlapping geo-economic shocks clouding the future, I believe that risk management is now the most sensible approach to monetary policy responses; this has now been articulated by multiple central banks and academic research. 30. The chances of a policy mistake remain heightened given the two-way risks on the inflation-growth outlook. However, given the MPC forecasts on growth and inflation, and factoring in the elevated and rising inflation expectations, we must now closely monitor second order input cost transmission getting embedded in retail inflation. This will depend on the intensity and duration of the energy shock. Despite my concerns, I must cautiously note that, as of early June ’26, I do not see material signals of economic overheating. Hence, the policy repo rate is currently appropriate and a status quo at the June ’26 review is likely to have the lowest economic cost. 31. Based on this reasoning, I vote to keep the repo rate unchanged at this meeting. Given the fluidity of the macro-financial environment, it is also appropriate to retain the neutral stance. Statement by Prof. Ram Singh 32. This meeting of the MPC has happened at a critical juncture for the Indian economy. We are faced with a delicate balancing act of supporting resilient yet uneven growth while keeping a check on rising inflationary pressures in a highly volatile external environment. 33. In previous MPC deliberations, I advocated for an accommodative monetary policy (MP) stance. My position was rooted in a clear economic rationale: Headline CPI and core inflation were comfortably range-bound, but private capital expenditure and the working capital needs of MSMEs required support. Since the last MPC meeting, however, there have been material changes in the domestic price and growth trade-offs due to the persistence of the West Asia (WA) conflict and its implications. 34. Today, the global economy presents a complex mix of persistent inflation, elevated projections for crude oil and other commodity prices, volatile financial markets, and shifting monetary policies across major central banks. In April and May 2026, FPIs withdrew a net $1.8 billion from emerging market equities, even as the monetary policy paths of advanced economies remain uncertain. With the US Federal Reserve facing sticky services inflation and a resilient labour market, expectations for rate cuts have been pushed to late 2026 or early 2027. All these external factors directly impact our domestic policy options, and our policy response must evolve accordingly. 35. Below, I outline recent developments on the inflation and growth fronts, as well as the risk assessments that guided my decisions for this MPC meeting. Inflation 36. Brent crude prices, which averaged around US$67 per barrel during Jan-Feb 2026, have come under sharp upward pressure, settling in the $90- $ 100 per barrel range after spiking well above $100. RBI’s analysis indicates a clear relationship between energy prices and domestic inflation: If crude oil prices are higher by 10 per cent than the baseline, assuming full passthrough to domestic product prices, inflation could turn out to be higher by around 50 bps. Inflated crude import bill expands our CAD. 37. The WA disruptions are no longer confined to the shipping sector; they are affecting broader trade infrastructure. Longer transit times around the Cape of Good Hope have added approximately 10 to 14 days to voyages from Asia to Europe, raising insurance premiums for cargo vessels by nearly 50%. Freight rates along major maritime routes have increased by an average of 35% since January 2026.1 These factors, along with heightened uncertainty in commodity supply chains, have led to a spike in commodity prices beyond crude and its by-products. This, in turn, very likely will put pressure on input costs across India’s manufacturing sector. For instance, the price of imported natural gas and industrial metals—particularly copper and aluminium—rose by 12% year-on-year in May 2026. 38. The pressure on CAD from a war-inflated crude import bill and developments on the capital account front can compound the impact of imported inflation. As of April 2026, fuel inflation has remained modest due to the limited pass-through of the sharp spike in international energy prices to domestic retail prices. The CPI inflation has remained below the target. Core inflation is also well below 4%. Core inflation excluding precious metals has remained much lower at 2.1-2.2 per cent, as input cost pressures have not yet fully reflected in CPI, even though the pass-through of higher global energy prices is visible in several inputs such as commercial LPG, industrial raw materials, chemicals, rubber, and plastic products. 39. As we advance, the incoming data will inform the extent of the second-round impact of higher input costs on CPI inflation. At this point, CPI inflation for 2026-27 is projected to be 5.1 per cent with a peak at 5.9 per cent in Q3. Core inflation is projected at 4.7 per cent for 2026-27. Growth 40. Urban demand remains robust, supported by strong expansion in the services sector and a stable employment situation. The private consumption growth remains robust at 7.7% for FY26 (y-o-y). Recent data on a wide range of indicators, such as FMCG sales, passenger vehicle and tractor sales, credit growth to the household sector, and credit card spending, indicate the resilience of domestic demand so far. 41. Private sector capital expenditure has also shown signs of recovery in FY 26 Q4 across several sectors, including real estate and energy. On the exports front, services exports are holding up well. Goods exports recorded strong growth in April 2026, partly due to the price effect, though elevated freight and insurance costs remain a drag on exports. Overall, the economy is expected to register a real GDP growth at 6.6% in FY27. 42. While a 6.6% growth rate is the highest among major economies, it is a significant moderation from our recent performance – 7.7% in FY 26. Moreover, the impact of the looming uncertainty on the GDP components requires a careful approach to monetary policy. 43. For instance, capacity utilisation across manufacturing plants at 75.2% for Q4 FY26 has surpassed its long-term average (74.0%) and corporate balance sheets are healthy, yet corporates remain cautious. Broad-based private capital investment has been hit by heightened uncertainty stemming from external factors, including financial market volatility and uncertain global demand. The IIP showed a growth rate of 4.9% (y-o-y) in April 2026, down from 5.7% in the same month last year. It reflects rising input cost pressures and, perhaps more importantly, a risk-averse response to the impact of geopolitical factors on supply chains and global demand. 44. While the economy has withstood the conflict spillovers with limited impact so far, the strains are increasingly becoming visible. The El Niño weather phenomenon can significantly impact agricultural growth and rural demand. In such an environment, the MP should not dampen the modest but encouraging signs of a pick-up in private investment. We must design policy carefully to support growth without risking the unanchoring of inflation expectations. 45. In my view, there is no risk of inflation expectations getting unanchored. First of all, the central government has effectively kept retail energy prices in check through a partial and staggered pass-through of crude oil prices. The excessive refining capacity means that the crack spread for petroleum products in India is significantly less than the world average, limiting the impact of the WA crisis on a wide range of industrial inputs. Similarly, the centre’s decision to keep fertiliser prices stable will help ease the input cost pressures on agriculture. These factors will help moderate the second-round price effects. 46. On top of it, the crude oil prices seem to have stabilised. Given that the costs of WA conflict are compounding for the parties involved, the odds of a truce between the parties are increasing, an inference corroborated by data on crude futures and bond markets. Further, the domestically produced alternatives to imported inputs (such as ethanol blended petrol) and the diversification of critical imports have strengthened the economy’s resilience to external shocks. Further, sustained low level of core inflation indicates that there are no immediate broad-based demand pressures in the economy, other than those stemming from imported inflation and precious metals.2 47. Still, as long as the WA conflict persists and the impact of El Niño remains unquantified, it makes sense for the MP to retain all the flexibility needed to respond to evolving inflation and growth trajectories. A “neutral” stance provides the MPC with maximum operational flexibility without being constrained by previous commitments. If external shocks worsen or the second-round price effects spread widely, the neutral stance allows us to adjust policy to protect macroeconomic stability. 48. My long-term policy preference remains growth-supportive. The prevailing real interest rates arising from the present combination of the policy repo rate at 5.25 per cent and the inflation trajectory for the coming quarters make for a growth-supportive monetary policy. If the inflation-related risks resolve favourably—food inflation remaining stable, global oil prices stabilising below $80 per barrel, and the Federal Reserve avoiding hawkish decisions—in my view, the MPC will have the room to continue to be growth-supportive. 49. Accordingly, in this meeting, I vote to keep the policy repo rate unchanged at 5.25% and support maintaining the stance to “neutral”. Statement by Shri Indranil Bhattacharyya 50. The prolonging of the West Asia conflict without any meaningful resolution in sight has distinctly soured global economic sentiments since the April policy. The drifting trajectory of the conflict, with intermittent phases of intensification and ebbing, triggered risk-on and risk-off sentiments that heightened uncertainty and imparted volatility to financial markets. The continuing disruption of the supply chain and consequent sharp escalation of international energy prices is increasingly getting reflected in India’s import bill and wholesale inflation. 51. Notwithstanding active government interventions to facilitate supply availability, elevated energy prices along with persisting logistical challenges continue to pose risks to the domestic growth outlook. The projected deficiency in south-west monsoon may adversely weigh on agricultural activity and rural demand, although several ongoing Government initiatives on agriculture3 may partially mitigate the impact. In industry, high-capacity utilization and buoyant credit offtake suggest favourable prospects for investment. Services exports are expected to retain momentum, even as merchandise exports may be hampered by weak global demand and elevated freight and insurance costs. In view of these factors, GDP growth for 2026-27 has been trimmed by 30 basis points (bps) from 6.9 per cent projected in April 2026. 52. Headline CPI inflation at 3.5 per cent in April continued to remain below the 4 per cent target. Moreover, the March and April momentum of CPI core inflation remained subdued (0.2 per cent and 0.3 per cent, respectively) indicating that the transmission of energy price shocks and supply shortages is yet to reflect in core inflation. WPI inflation, however, increased sharply to 8.3 per cent in April from 3.9 per cent in March, driven by increases in energy and other industrial input prices. Although cost-push pressures are yet to manifest in retail inflation, the possibility of lagged but higher pass-through along with adverse weather and monsoon forecasts are shaping the inflation outlook. Accordingly, CPI inflation projection for 2026-27 has been revised upwards from the April policy by 50 basis points to 5.1 per cent – primarily due to the assumption of higher average oil prices in 2026-27 and the IMD’s projection of a below normal southwest monsoon. 53. Flexible inflation targeting is a framework best characterised as constrained discretion, in which monetary policy is anchored to a numerical target but retains the scope to accommodate shocks. This flexibility is especially important during periods of high uncertainty. The tolerance interval is one component of constrained discretion – target ranges, and, in some cases, tolerance bands, can improve the anchoring of inflation expectations relative to point targets.4 Moreover, policy discretion is increasingly exercised on the target horizon. Since 1990, evidence from 26 inflation-targeting central banks shows that while strict adherence to the target have become inviolable, inflation converges to the target over a longer horizon.5 54. Inflation projections are subject to several uncertainties in the present context. While WPI inflation has spiked, one needs to wait for its pass-through to CPI inflation. Moreover, the spatial and temporal distribution of monsoon, which is critical for crop outlook, is not yet known. The impact of the projected El Niño conditions is conditional on the Indian Ocean Diapole (IOD) situation, which may partly mitigate the impact. Furthermore, the government has already undertaken several measures to moderate the impact of a deficient monsoon. While demand-pull inflation may call for pre-emptive action to effectively anchor inflation expectations, cost-push inflation induced by supply shocks warrants greater caution – gradualism – in policy making. In view of these factors, I feel it is prudent to wait for greater clarity to emerge from the data before deciding on any policy action. Accordingly, I vote for a pause on the policy rate while retaining the neutral stance. Statement by Dr. Poonam Gupta 55. Global uncertainties have continued to persist since the last policy in April 2026. While countries have found ways to secure supplies of energy and other related products, they have also eroded their strategic reserves, and have increasingly been passing on higher energy costs to consumers. 56. India too has adopted a somewhat similar approach to the ongoing shock. Supplies have been secured from diverse sources, albeit at higher prices, compounded by higher shipping and insurance costs, and exchange rate depreciation. Prices have been partially passed through to the consumers. 57. These developments have led to a revision in our forecasts of growth and inflation. We have had to move closer to the alternate scenario outlined in the Monetary Policy Report (April 2026), which assumes crude oil prices at around US$95/barrel. GDP growth is now expected to slow down to 6.6 per cent in 2026-27, while average headline inflation may edge up to 5.1 per cent. Deceleration in growth is projected to be the sharpest in the second quarter of 2026-27, with a revival in the last quarter. Inflation is projected to accelerate most in the third quarter, followed by some moderation in the last quarter. A large part of the projected acceleration in inflation is concentrated in fuel and food components with some pass-through to core inflation through the input cost channel. 58. Overall, the Indian economy seems to have held up well despite the shocks: there is sufficient liquidity in the system; credit growth continues to be strong at about 16 per cent; most of the sectoral outlooks and high frequency indicators are holding up; and the overall macroeconomic and financial sector stability has been sustained. The IMF’s latest Fiscal Monitor has singled out India as an economy where public debt as a per cent of GDP is projected to decline over the next few years, based on high nominal GDP growth, fiscal consolidation, and better composition of expenditure. 59. How should these developments guide monetary policy? I feel we ought to wait a bit more for global as well as weather related uncertainties to play out over the coming months, before taking a call on whether and when to reverse the policy cycle. 60. This is for two reasons. First, at the current juncture, with growth projected to decelerate and inflation yet to become entrenched, I do not see a case for policy tightening to rein in inflation or inflationary expectations. If anything, it could make the economic pain of the ongoing supply shock sharper. 61. Second, once the West Asia conflict is resolved, the outlook, both for India as well as globally, could improve rapidly warranting a fresh look at the inflation-growth dynamics. Therefore, it would be prudent to adopt a wait and watch approach rather than make an early or preemptive policy pivot. 62. Hence, I vote for the status quo, that is, to keep the policy repo rate unchanged at 5.25 per cent. I also propose to retain the stance at neutral, signaling that the future course of policy action should be data dependent. Statement by Shri Sanjay Malhotra 63. On the whole, our economic situation is quite strong and healthy vis-à-vis many of our peers. We are in a much better position today not only in terms of the current shock but also with respect to all earlier shocks. We are one of the fastest growing major economies and our inflation has been benign in the past year. 64. While headline inflation continues to remain within the target, CPI inflation for 2026-27 is now projected to be above target at 5.1 per cent. The increasing inflation trajectory for 2026-27 with its peak of 5.9 per cent in Q3 – close to the upper tolerance level of 6 per cent – may suggest the need for monetary policy action. However, I would prefer to wait and watch for the following reasons. 65. One, there is high uncertainty in the assumptions made for projections of both inflation and growth on account of several reasons – the duration of the conflict and the disruption in supply chains, the intensity and geographical spread of monsoons and their impact on energy, food and other commodity prices. 66. Two, while headline inflation is projected to be on the higher side of the inflation tolerance band, core inflation for 2026-27 is projected at 4.7 per cent for 2026-27. Excluding precious metals, the core inflation is even lower than the target. 67. Three, most of the increase in the projected headline inflation between April policy and now is driven by food and fuel, which is supply driven. It may be a change in price level, which may or may not get generalized. 68. Four, even though it is inflation outlook which is more relevant for monetary policy, current inflation merits attention, especially when the outlook is clouded. Headline inflation continues to be within target in April. Most of the observed increase in inflation is on account of higher food inflation. Core inflation also remained contained, suggesting that underlying inflation pressures remained subdued. 69. Having said this, we need to be watchful of the inflation trajectory. Going forward, revision in retail prices of petrol and diesel in May would lead to higher fuel inflation in the coming months. While the near-term outlook for food prices remains favourable on account of a good rabi crop and adequate stocks, risks have amplified, especially from a below normal monsoon as predicted by the IMD and likely El Niño conditions. Average crude prices have increased sharply from what were assumed in April; WPI for April is elevated; consequently, cost pressures from higher energy and other input prices could also feed into core inflation. Therefore, we would continue to be data dependent and remain vigilant about inflation getting generalized, which can unhinge inflation expectations. 70. To summarise, I would prefer to adopt a “wait and watch” approach. Accordingly, I vote for a status quo on the policy rate while retaining the neutral stance. We should remain watchful and wary about the generalization of inflation in the coming months. (Brij Raj) Press Release: 2026-2027/497 1 The Drewry World Container Index that tracks spot market container freight rates across major East-West shipping routes has risen to levels not seen since the supply disruptions of 2021–2022. 2 Excluding precious metals, core inflation remained much lower at 2.1-2.2 per cent. 3 Crop diversification, water conservation, climate-resilient agricultural practices, and the adoption of short-duration crop varieties. 4 Ehrmann, M. (2021). Point Targets, Tolerance Bands, or Target Ranges? Inflation Target Types and the Anchoring of Inflation Expectations. Journal of International Economics, 132(C). 5 Borio, C. and Chavaz, M. (2025). Moving Targets? Inflation Targeting Frameworks, 1990–2025. BIS Quarterly Review, March. |